Tax in China M&A – Lexology

21 min readIntroduction

The tax system of the People’s Republic of China has evolved over the past 70 years. At the beginning of the founding of the republic in 1949, China only imposed a few types of taxes, as before 1978 most enterprises were either state-owned or collectively owned by a group of farmers. In the mid- and late-1980s, China reformed its tax system and started to impose enterprise income tax on state-owned and collectively owned enterprises, in addition to collecting income tax from privately owned enterprises.

In the following 20 years or so, China also gradually revamped its indirect taxation of enterprises, including state-owned and collectively owned enterprises. From early 2018, China began to levy VAT on revenue generated by commercial enterprises from the provision of services, repealing the business tax (a gross receipts tax on services). Thus, since early 2018, the provision of services, the disposition of intangible assets and the sale or importation of products have been subject to VAT across the board. China also imposes consumption tax on the production, sale and importation of certain specifically listed luxury goods. Furthermore, China imposes transaction taxes such as stamp duty and deed tax for the sale and purchase, exchange or gifting of real property.

This chapter is not intended to cover all taxes that China imposes on taxpayers, or to give an overview of China’s taxation history. Instead, it focuses on the taxes in China that impact China-inbound foreign direct investment, cross-border mergers and acquisitions in particular, and provides some observations on tax structuring or restructuring issues.

Brief overview of major PRC taxes

Enterprise income tax

Income taxation of enterprises in China is now governed by the Enterprise Income Tax Law of the People’s Republic of China, and the Detailed Regulations for the Implementation of the Enterprise Income Tax Law of the People’s Republic of China, and supplemented by various tax circulars or bulletins issued by the PRC Ministry of Finance, the State Administration of Taxation (SAT) or both (collectively, the Enterprise Income Tax Law).

China is a jurisdiction that imposes corporate income tax based on both the tax residence of the taxpayers and source of income generated by the taxpayers. In other words, the income tax consequences of being a Chinese taxpayer will vary depending on whether such taxpayer is (or is deemed to be) a tax resident of China; and if not, whether the income in question was sourced from within China. Although it takes pages to explain how China’s sourcing rules work, the rule of thumb is that the revenue would be sourced from within China, if a taxpayer:

- produces or sells products in China, or imports goods into China;

- provides services within China;

- licenses or transfers technology, trademarks or other IP rights to a licensee that will use such IP in China; or

- derives passive income (eg, dividends, interest and capital gains) other than royalties for the use of IP rights.

Resident versus non-resident

Under the Enterprise Income Tax Law, companies that were incorporated in the PRC and companies that were incorporated outside the PRC but are deemed to have a place of effective management[2] in the PRC (collectively, resident enterprises) are subject to enterprise income tax (EIT) at the general rate of 25 per cent on a worldwide basis. Companies incorporated outside the PRC and not deemed to have a place of effective management in the PRC (non-resident enterprises) would be subject to Chinese EIT only with respect to their income attributable to:

- their respective business establishment[3] (BE) through which they carried on their business activities in the PRC; or

- the passive income, such as capital gains, dividends, interest and royalties they receive from companies or individuals in the PRC.

Taxation of resident enterprises

Resident enterprises, such as foreign invested enterprises (which include wholly foreign owned enterprises (WFOEs), Sino foreign equity joint ventures and Sino foreign cooperative joint ventures), are subject to EIT on their worldwide income irrespective of whether such income was sourced from within or outside China. Where a portion of a resident enterprise’s income was sourced from overseas (eg, dividends, interest and royalties received from a non-resident enterprise), the Enterprise Income Tax Law allows the resident enterprise to credit foreign income taxes paid in respect of such foreign-sourced income against EIT that would otherwise be payable if such income were sourced from within China and had been subject to EIT at 25 per cent.

As this book is focused on legal, tax and other issues of China-inbound M&A transactions, this chapter does not discuss in detail other aspects of income taxation of resident enterprises.

Income taxation of non-resident enterprises

Business presence – active income

Pursuant to the Enterprise Income Tax Law, non-resident enterprises are subject to 25 per cent EIT on their (deemed) taxable income in respect of their active income from carrying out business in China through a place or establishment therein. ‘Place or establishment’ includes a management office, business establishment, representative office, factory, site for extraction of natural resources, place where services are provided, site for operating a construction, installation, assembly, repair or exploration project, and the place of business of an agent who has the authority to habitually sign contracts and exercises authority to conclude contracts on behalf of the non-resident enterprise; however, unlike resident enterprises, non-resident enterprises would generally be subject to income tax on a deemed profit basis (generally 30 per cent, but in some cases up to 50 per cent of their gross revenue would be the deemed profit), or in the case of PRC representative offices of non-resident enterprises, most commonly on a cost-plus basis.[4]

No business presence – passive income

Under the Enterprise Income Tax Law, non-resident enterprises without a place or establishment in China but deriving ‘income from sources within China’ are subject to a 10 per cent withholding tax. ‘Income from sources within China’ of non-resident enterprises without a place or establishment in China typically includes the following:

- after-tax profits (dividends) received from enterprises within China;

- interest derived from within China on deposits, loans, bonds, advance payments made provisionally on another’s behalf or deferred payments;

- rental on assets leased to and used by parties in China;

- royalties generated by providing patent rights, proprietary technology, trademark rights, copyright and other such rights for use in China;

- earnings from assigning assets, such as buildings, structures and their auxiliary facilities and land-use rights; and

- other income derived from inside China and stipulated as taxable by the Ministry of Finance and the SAT.

Special rules applicable to representative offices

Subject to exemption provisions under the applicable bilateral tax treaty, China imposes EIT on representative offices of non-resident enterprises in China (ROs) (and VAT – discussed later) with respect to the following activities:

- engaging in liaison activities, negotiations and introductory services performed in China on behalf of clients of their respective head offices located outside China;

- conducting market surveys, collecting commercial information and providing consulting services in China on behalf of clients regardless of whether the clients pay for such services on a retainer or other basis; and

- engaging in liaison activities and negotiations, intermediation and introductions in China on behalf of other companies.

In the above three scenarios, it does not matter whether the clients or third-party companies pay a services fee directly to the RO or its head office overseas. However, an RO would be exempted from income tax (and VAT):

- if the head office of the RO is a foreign manufacturer and the RO acts solely for its head office, by limiting its activities to conducting market surveys, promoting the sale of the head office’s products in China or conducting other business liaison for the head office; or

- if it earns income for services performed primarily outside of China on behalf of enter- prises located within China.

In theory, ROs can be taxed using:

- the ‘actual revenue and expense’ method;[5]

- the ‘deemed profits’ method;[6] or

- the ‘cost-plus’ method.[7]

However, in practice, except for ROs of foreign law, accounting and consulting firms, most ROs have been taxed on a cost-plus basis over the past three decades.

Value added tax

China’s VAT system was modelled after the European VAT systems but is somewhat different from its European counterpart. Two of the major differences between these two sets of VAT systems are:

- only large-scale VAT payers[8] are allowed to offset their input VAT against their output VAT; and

- China’s VAT regulations do not allow VAT exemption for export goods from the beginning of the production chain through the exportation. Instead, they only exempt the ultimate exporters from VAT when the products are actually exported, while requiring the exporters to claim back their input VAT after exports and often at a rate lower than the VAT rate several months later.

In general, VAT is imposed on revenue generated from the sale of goods (eg, physical assets) or intangible assets, as well as the provision of processing, repair, maintenance, transportation, professional service and other services. VAT is also payable in respect of imported goods, unless there is a specific VAT exemption applicable to the imported goods.

The standard VAT rate for sale of goods is 13 per cent, while a 9 per cent VAT rate applies to the sale of granted land-use rights or other real property, as well as certain specifically listed services, and 6 per cent VAT is imposed on revenue from provision of services.

Land appreciation tax

Land appreciation tax is imposed on the incremental value of the transfer of state-owned land-use rights, above-ground structures and their attached facilities, and is collected at the specified tax rate. The taxpayer files the tax returns with the competent tax authority where the real estate is located, within seven days of the execution of the real estate transfer contract, and pays the land appreciation tax within the time limit designated by the tax authority.

Generally, the following four level progressive tax rates shall be applied on the land appreciation:

- for the part of the appreciation amount not exceeding 50 per cent of the sum of deductible items, the tax rate is 30 per cent;

- for the part of the appreciation amount exceeding 50 per cent, but not exceeding 100 per cent, of the sum of deductible items, the tax rate is 40 per cent;

- for the part of the appreciation amount exceeding 100 per cent, but not exceeding 200 per cent, of the sum of deductible items, the tax rate is 50 per cent; and

- for the part of the appreciation amount exceeding 200 per cent of the sum of deductible items, the tax rate is 60 per cent.

The above-mentioned deductible items include:

- the sum paid for the acquisition of granted land-use rights;

- costs and expenses for the development of the land;

- costs and expenses for the construction of new buildings and facilities, or the assessed value for used properties and buildings on the land;

- taxes related to the transfer of real estate; and

- other deductible items as stipulated by the Ministry of Finance.

The relevance of land appreciation tax in the context of M&A transactions depends on whether the tax is applicable to the parties to the transactions in an equity or share deal (as opposed to an asset deal). In other words, whether the land appreciation tax applies is dependent on there being a transfer of ownership of real property as part of the transaction.

Deed tax

Deed tax is payable by the grantee, transferee or purchaser under one of the following scenarios:

- acquisition of granted land-use rights from the state;

- transfer of granted land-use rights, either by sale, exchange or gifting; or

- sale and purchase, exchange or gifting of real property situated on land.

Contribution of capital to a company in the form of granted land-use rights, or real property situated on such granted land, settlement of debt by transfer of property title to the creditor, or obtaining title to land upon winning a bid for granted land-use rights to a parcel of land shall be deemed to be a taxable transfer.

The deed tax rate ranges from 3 per cent to 5 per cent, to be adjusted by provincial governments, and the four municipalities directly under the Central People’s Government.

Stamp duty

China also levies stamp duty on certain specifically listed legal documents. The imposition of stamp duty is primarily based on the Provisional Regulations of the People’s Republic of China on Stamp Duty, issued by the State Council pursuant to authorisation by the National People’s Congress (NPC), China’s legislature. However, many foreign investors are not familiar with China’s stamp duty and often overlook it in the M&A context.

The following categories of documents are subject to stamp duty:

- documents issued for purchase and sale transactions, general contracting or processing, property leasing, commodity transportation, storage and custody of goods, loans, property insurance, technology contracts and other documents of a contractual nature;

- documents of transfer of property title;

- accounting books of businesses;

- documentation of rights or licences; and

- other documents determined by the Ministry of Finance to be taxable.

The table below provides a detailed description of taxable instruments and documents and the corresponding stamp duty rate as of 2019.

|

No. |

Taxable |

Scope |

Tax rate |

Taxpayers |

|---|---|---|---|---|

|

1 |

Purchase and sales contracts |

Contracts for supply, pre-sales, procurement, combined purchase and cooperative manufacturing arrangement, compensation trade, bartering trade, etc |

0.03{14cc2b5881a050199a960a1a3483042b446231310e72f0dc471a7a1eddd6b0c3} of value of purchases |

Parties to the contract |

|

2 |

Processing contracts and contracts for hired work |

Contracts for processing, custom build, repair and maintenance, printing, advertisement, surveying or testing, etc |

0.05{14cc2b5881a050199a960a1a3483042b446231310e72f0dc471a7a1eddd6b0c3} of the revenue generated from these contracts |

Parties to the contract |

|

3 |

Engineering and construction, project survey and design contracts |

Contracts for survey and design |

0.05{14cc2b5881a050199a960a1a3483042b446231310e72f0dc471a7a1eddd6b0c3} of service fees paid and received |

Parties to the contract |

|

4 |

Construction and installation contracting |

Contract for construction and installations |

0.03{14cc2b5881a050199a960a1a3483042b446231310e72f0dc471a7a1eddd6b0c3} of contracted amount |

Parties to the contract |

|

5 |

Property leasing contracts |

Contracts for leasing of buildings, vessels, aircraft, motor vehicles, machinery, devices and tools, as well as equipment |

0.1{14cc2b5881a050199a960a1a3483042b446231310e72f0dc471a7a1eddd6b0c3} of the lease contract. Any amount less than 1 yuan to be stamped as 1 yuan |

Parties to the contract |

|

6 |

Goods transportation contracts |

Contracts for transportation via civil aviation, railway transportation, maritime shipping transportation via inland waterways, land transportation and transportation using any combination of the above transportation means |

0.05{14cc2b5881a050199a960a1a3483042b446231310e72f0dc471a7a1eddd6b0c3} of the transportation fee |

Parties to the contract |

|

7 |

Warehousing and safekeeping contracts |

Contracts for warehousing and/or safekeeping |

0.1{14cc2b5881a050199a960a1a3483042b446231310e72f0dc471a7a1eddd6b0c3} of warehousing and/or safekeeping fees |

Parties to the contract |

|

8 |

Loan contracts |

Contracts entered by banks and other financial institutions and borrowers, except interbank offer loan agreements |

0.005{14cc2b5881a050199a960a1a3483042b446231310e72f0dc471a7a1eddd6b0c3} of the loan amount |

Parties to the contract |

|

9 |

Property insurance contracts |

Insurance contracts for property, bonding guarantee, surety and credit undertaking, etc |

0.1{14cc2b5881a050199a960a1a3483042b446231310e72f0dc471a7a1eddd6b0c3} of the insurance premium amount |

Parties to the contract |

|

10 |

Technology contracts |

Contracts for technology development and transfer, consulting and other services |

Stamping as 0.003{14cc2b5881a050199a960a1a3483042b446231310e72f0dc471a7a1eddd6b0c3} of the indicated amount |

Parties to the contract |

|

11 |

Property transfer contracts |

Transfer documents for property ownership and copyrights, trademark rights, patents, the right to the use of proprietary technology; contracts for land-use rights grant and transfer, and other title transfer documents |

0.05{14cc2b5881a050199a960a1a3483042b446231310e72f0dc471a7a1eddd6b0c3} of the amount indicated |

Parties executing the document or documents |

|

12 |

Accounting books for business operations |

Accounting books used for production and business operations |

For accounting books for recording funds received by the taxpayer: 0.05{14cc2b5881a050199a960a1a3483042b446231310e72f0dc471a7a1eddd6b0c3} of the total amount of the original value of fixed assets and self-owned working capital; for other accounting books: 5 yuan each |

Businesses with accounting books |

|

13 |

Certificates and licences |

Title certificates in respect of ownership of buildings; business licences issued by competent authorities for business operations; registration certificates for trademarks, patents and land-use rights issued by the competent authorities |

5 yuan per document |

Grantee |

China’s tax legislation and rule-making

China is a quasi-federal jurisdiction in that, with a few exceptions, all nationwide law, administrative regulations and rules are promulgated by the national legislature, the NPC or its Standing Committee, where applicable (or the State Council or one or more of the departments thereunder). However, it is different from the US federal system in that each of the provinces does not have any legislative power, and only autonomous regions such as Inner Mongolia have limited power to promulgate local statutes governing matters containing certain affirmative actions that create special benefits for minority peoples in the respective autonomous regions.

In China, laws such as the Enterprise Income Tax Law are promulgated by the NPC, while the implementing regulations for each national law would always be supplemented by implementing regulations issued by the State Council pursuant to the NPC’s authorisation or rules and other written interpretations (ie, circulars issued by the competent department under the State Council). As a matter of practice, each competent department under the State Council proposes new legislation or amendments to an existing law (together with the proposed implementing regulations for the new law or amendments to the existing implementing regulations, as the case may be) to the State Council.

Chinese tax implications for foreign investments Greenfield investment projects

At the beginning of China’s opening to foreign investment in the late 1980s and early 1990s, almost all foreign investments in China were in the form of establishing either an equity joint venture or a contractual joint venture; there were very few WFOEs. Back then, there were three separate tax laws, each governing income taxation of each type of foreign invested enterprise. Essentially, under China’s previous separate income tax law for each type of foreign invested enterprise, equity joint ventures, contract joint ventures and WFOEs and foreign companies doing business in China were taxed differently and with varying rates. Under the Enterprise Income Tax Law, all resident enterprises and non-resident enterprises with active income from China are subject to the same tax rate of 25 per cent.

Contractual joint ventures that were formed as quasi-partnerships, and are very rare nowadays, have been treated as partnerships for tax purposes. The foreign party, parties or corporate partners of contractual joint ventures have been essentially treated as non-resident enterprises of China, and the foreign party, parties or partners to contractual joint ventures are now subject to Chinese EIT at 25 per cent on a deemed profit basis in respect of their active income from carrying on business activities through a BE under Chinese domestic law or a permanent establishment under an applicable tax treaty, or a 10 per cent withholding tax on their passive income such as dividends, royalties, interest and capital gains received from sources within China.

In addition to the EIT, resident enterprises and non-resident enterprises are subject to VAT in respect of importation and sale of goods, provision of services and transfer and licensing of IP rights for use by Chinese licensees, sale or leasing of real property, and sale of other intangible property. VAT and other indirect or transaction taxes are not covered by bilateral tax treaties that China entered into with other countries.

Tax structuring prior to investments

As in all cross-border investment projects, pre-investment tax structuring is absolutely necessary, as the tax consequences affect the bottom line of the investment projects, and may render such an investment project financially infeasible or less financially rewarding for the investors. Given that the corporate income tax rate in China is fixed, except for some tax holidays, it is critical for China-inbound investors to put in place effective tax structures to minimise the aggregated income tax burden resulting from both economic double taxation and jurisdictional double taxation.

One typical example of economic and jurisdictional double taxation of the same income is where China imposes a 25 per cent tax on the profits of a resident enterprise, and generally a 10 per cent withholding tax on dividends to be paid to the non-resident enterprise shareholder out of the after-tax profits of the resident enterprise. On top of the 25 per cent and then 10 per cent EIT, the home country of the non-resident enterprise concerned, for example the United States, would also impose corporate income tax on the dividends received by the non-resident enterprise from the resident enterprise in China (though in countries like the United States, in the absence of the US–China tax treaty, the Internal Revenue Code would unilaterally allow foreign tax credits to the US company that receives dividends from the resident enterprise that paid dividends).

While economic double taxation is merely a Chinese domestic law issue, and such double taxation can only be done away with pursuant to Chinese domestic law, bilateral tax treaties between China and other countries would help eliminate most of the double taxation resulting from cross-border investment and movement of goods and services (ie, jurisdictional double taxation). Hence, treaty shopping, in other words, investing from a tax jurisdiction (eg, Hong Kong) whereby a lower withholding tax rate on dividends, interest, royalties and capital gains would apply, has been a common practice. From the late 1990s to the early 2000s, Mauritius and Barbados were popular jurisdictions for foreign investors to incorporate intermediate holding companies for holding investments in Chinese operating companies (equity joint ventures, cooperative joint ventures or WFOEs), as each of these two countries had a tax treaty that exempted the 10 per cent Chinese withholding tax on capital gains realised by intermediate holding companies in these jurisdictions from disposing their equity interest (shares) in the underlying operating companies in China. After China entered into a new bilateral tax treaty with these two countries respectively, doing away with the withholding tax exemption for capital gains, foreign investors now tend to choose Hong Kong or Singapore as the jurisdiction where they would form their intermediate holding companies.

In any event, in investing in China through an intermediate holding company or multiple-layer intermediate holding companies, foreign investors’ main objective is to minimise the overall income tax burden that would result from cross-border investment and business activities, thereby maximising the bottom line of the investment and business operations in China. This pre-investment tax structuring is critical both in greenfield projects and in M&A transactions whereby the acquiring party directly or indirectly purchases equity interest (shares) of the desired Chinese target.

Tax structuring – lessons learnt

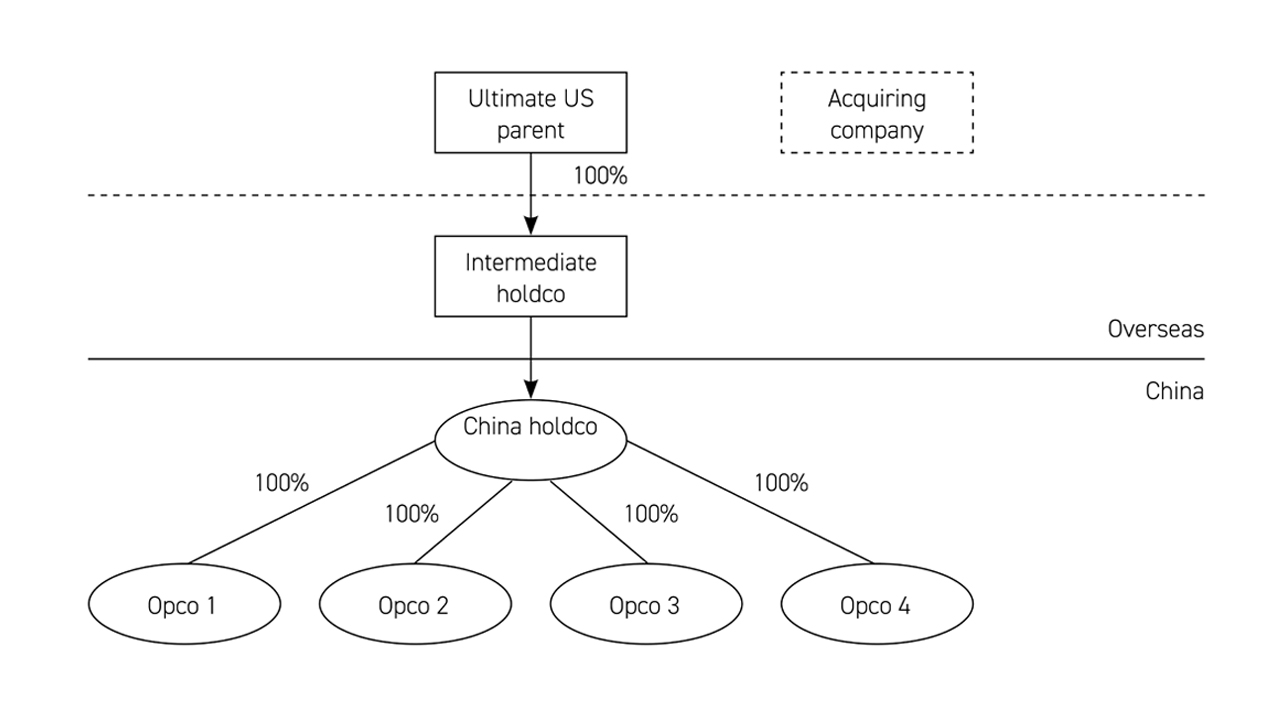

In the case of some foreign investors, the investment and tax structure was put in place by utilising an intermediate holding company in one of the above favourable jurisdictions, but the tax structuring within China was overlooked. One example of this failed tax structure is illustrated in the chart below.

Tax treaties do not address and cannot be invoked to address the economic double taxation resulting from the two-tiered Chinese company structure as illustrated above. The catastrophic result is that the capital gains would be taxed at 25 per cent rate in the hands of the Chinese investment holding company (China holdco), and again at 10 per cent rate (in the form of with- holding tax) in the hands of the Barbados intermediate holding company, if the foreign investor in the above hypothetical case sells one line of its business scattered among the operating companies underneath the China holding companies.

The foreign investor in the above hypothetical case could have avoided the 25 per cent EIT on the capital gains if, prior to the sale of the business line, it had conducted tax restructuring, moving and consolidating the line of business to one or two subsidiaries of the China investment holding company, and caused the holding company to transfer its equity interest in those subsidiaries to the intermediate holding company under China’s tax-free reorganisation rules. Or even better, if the foreign investor had initially created a parallel investment holding structure whereby an offshore intermediate holding company directly holds equity interest (shares) in the operating companies, which are exclusively or principally engaged in one line of the foreign investor’s business.

Taxes applicable in the context of M&A

M&A transactions involving Chinese operating companies could be dramatically different, depending on whether the contemplated acquisition or merger will be an asset deal or equity deal – in other words, whether the M&A target is the equity or shares of a company or all or part of the assets of a company. If it is an equity deal, no legal title to the assets of the target company will change hands; instead, only the equity or shares of the target company will be bought and sold. In the case of an asset deal, all or part of the assets of a company would be sold to the buyer or one of the offshore buyer’s affiliates in China.

Equity deal

Under an equity deal, the acquiring company would purchase shares of the target company or companies that are Chinese resident enterprises (an onshore equity deal), or shares of the intermediate holding company in an offshore jurisdiction (an offshore equity deal), thereby indirectly acquiring the equity of the target company in China. Furthermore, under an onshore equity deal, since only the equity in the target company will change hands, indirect taxes such as VAT and transaction taxes such as land appreciation tax and deed tax (which are applicable to the sale and purchase, exchange or gifting of real estate) can be avoided.

Where the selling company in an equity deal is a resident enterprise with a non-resident shareholder, the applicable taxes would be 25 per cent EIT on a net basis payable by the resident enterprise, and 10 per cent withholding tax on the non-resident shareholder of the outgoing dividends paid out of gains from disposition of such shares. If the seller is a non-resident enterprise, then the seller is required to pay a 10 per cent withholding tax in respect of its capital gains derived from disposition of such equity or shares. In both scenarios described above, a 0.05 per cent stamp duty would be payable by both the seller and the buyer.

A further Chinese capital gains tax complication results from a foreign investor’s sale of its shares of the offshore intermediate holding company, which owns 100 per cent of the equity interest in its WFOE or part of the equity interest in a joint venture, thereby accomplishing the objective of disposing its equity interest in the WFOE or joint venture indirectly (indirect share transfer). Under Chinese tax rules governing indirect share transfers (the Enterprise Income Tax Law and SAT Bulletin 7 [2015]), with a few exceptions, all indirect share transfers would be collapsed into one single onshore transaction as if the foreign investor had directly transferred its equity interest in the WFOE, and a 10 per cent withholding tax would be imposed on the capital gains realised by the transferor.[9] However, no stamp duty would be due and payable, since there is not a direct transfer of legal ownership of the equity in interest in the WFOE.

Asset deal

In the case of an asset deal, the seller would sell, or cause its Chinese subsidiary to sell, all or part of its assets to another resident enterprise, as part of a bigger global M&A deal or pursuant to a simple onshore asset deal between the seller and buyer. Given that physical and intangible assets will be bought and sold in an asset deal, in addition to EIT on the gains from selling the assets, the following taxes may, depending on the particular circumstances of each transaction, also be applicable:

- 13 per cent VAT for the sale of the inventory, though both the seller and buyer would be allowed to offset their input VAT against their output VAT allowed;

- 6 per cent VAT on the revenue from transfer of the intellectual property, and imputed goodwill associated with the sale of assets;

- 2 per cent effective VAT on the proceeds from sale of physical assets (eg, manufacturing equipment);

- land appreciation tax at the applicable rate and payable by the seller of real estate;

- deed tax payable by the buyer at the applicable rate (generally 3 per cent to 5 per cent) as determined by the local government having jurisdiction over the real property to be sold to the buyer; and

- 0.05 per cent stamp duty payable by the resident enterprise buyer on the increased amount of the registered capital (equivalent of paid-in capital) resulting from assets purchased or acquired in an M&A transaction.

Recent tax enforcement trends

The SAT, which has branches and sub-branches at the provincial, municipal and county levels, is the central government agency charged with administering collection of taxes. In addition to issuing various announcements and bulletins guiding local branches and sub-branches in tax collection, the SAT also decides on the focus of tax enforcement efforts. In recent years, the SAT and its local branches and sub-branches have expanded significant resources in investigating tax compliance in indirect share transfer transactions, identifying and conducting transfer pricing audits and spearheading tax audits of selected industries, such as movie production, where tax evasion was rampant.

The SAT has also been challenging the legality and deductibility of inter-company payables between multinational corporations’ (MNC) headquarters and Chinese subsidiaries since the mid-1980s, when it noticed that a number of MNCs had put in place inter-company charges, and viewed such arrangements as a way of transferring out of Chinese pre-tax profits that would otherwise be taxable in the hands of the Chinese subsidiaries of these MNCs.

Concluding remarks

Over the past 40 years or so, China’s tax system has evolved into a fairly complex system, under which a direct (income) taxation regime coexists with an indirect tax scheme containing VAT and consumption tax, and a parallel transaction taxes net. This complex tax system, coupled with the involvement of multiple tax jurisdictions in relation to China-inbound investment, makes thoughtful and thorough tax planning and both pre- and post-investment tax structuring a must. In the absence of such tax planning and structuring, foreign investors will no doubt eventually encounter Chinese tax problems of one kind or another that are difficult to solve, and may find themselves forced into a corner where they have no choice but to pay unnecessary taxes that could have been legally avoided in the first place.